Deep Sea Mining part 3

financial and strategic considerations

This is the final installment of a three-part series on Deep Sea Mining by materials chemist Claire Cobley. See Part I for an introduction to deep sea mining and the influence of batteries on the demand for the metals it provides, and Part II for an introduction to metallurgical processing, as well as a discussion of how the environmental impact of processing ores from land compares to nodules from the sea.

Running the Numbers

Beyond environmental considerations, it is easy to wonder if deep sea mining is truly worth all the hassle and expense. Building new types of robots and equipment, shipping nodules across vast swaths of ocean, developing new processing flowsheets, all these things are expensive and add risk compared to existing methods.

To reassure investors and others, companies in this space have published technoeconomic analyses (TEAs) of their proposed approaches. The high level of detail illustrates just how many factors there are to optimize, yet also makes it clear that a successful team could bring in substantial revenues. Studies by the International Seabed Authority indicate that the Clarion-Clipperton Zone (CCZ) in the Pacific Ocean contains 21 billion tonnes of polymetallic nodules at an estimated value of 320 to 1,100 USD/tonne, indicating a value of anywhere between 7 and 20 trillion USD.

It is also notable that much of the cost and risk has nothing to do with the fact that the nodules are harvested from the deep sea. Significant costs come from the processing stage, and one of the most uncertain factors in determining whether the project will be financially successful is the fluctuating market price of metals. These costs and risks also exist for land-based projects, and the presence of multiple metals in nodules could soften the blow of price drops of a specific metal.

Speed

Although metal price and demand projections vary in the long term, many people have expressed particular concern about our ability to extract critical minerals in the short to medium term due to society’s rapid electrification. Building a new land-based mine takes an average of 16 to 18 years, so new discoveries will not ameliorate this concern.

Because nodules must be transported to land regardless, deep-sea mining companies often propose processing their initial loads of nodules at existing facilities. If this plan proves viable at scale, metals harvested from the ocean could be a reality sooner than many expect. The Metals Company and PAMCO in Japan recently tested this setup with a 2,000-tonne pilot run, which was intended to demonstrate the technical compatibility of existing kilns, paving the way for a targeted commercial throughput of 1.3 million tonnes of wet nodules annually.

However, ‘technical compatibility’ does not equal ‘immediate production.’ Years-long delays in reaching optimal recovery are common even for land-based mines with familiar ores; new processing plants take 2.5 years to reach intended throughput even after production begins. Although pilot studies have been informative, uncertainties still remain about how polymetallic nodules will behave at true industrial scale. Experts believe that a ramp-up period will be unavoidable as companies move from short-duration tests to continuous, year-round operations.

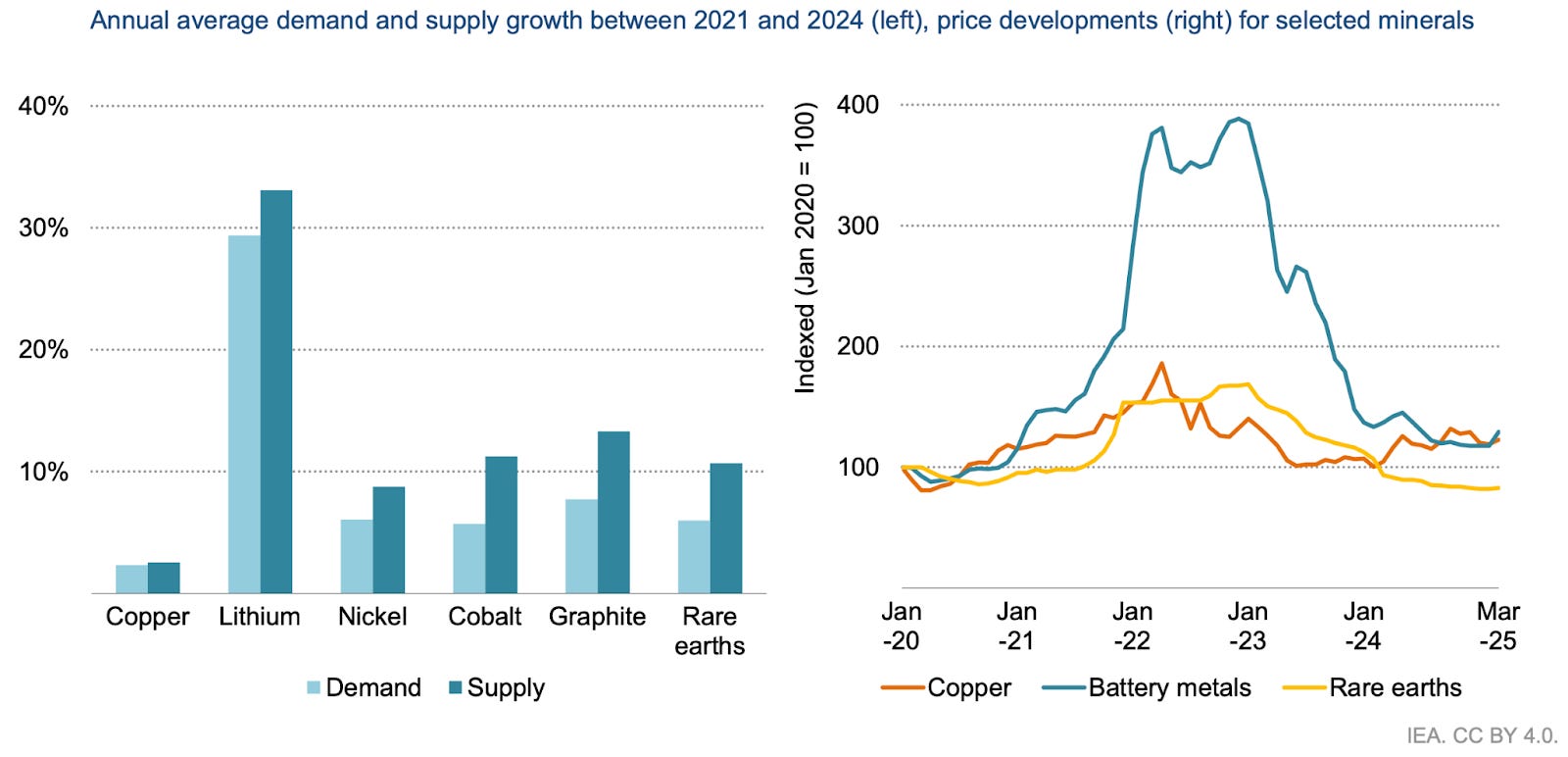

Furthermore, deep sea mining is not the only creative response to potential metal shortages, and high prices have a tendency to motivate people to find new solutions. Existing land-based facilities, particularly nickel operations in Indonesia, have successfully ramped up production to meet, and in some cases exceed, rising global demand. As shown in the image below, this surge in supply has led to notable price drops in battery metals.

Politics

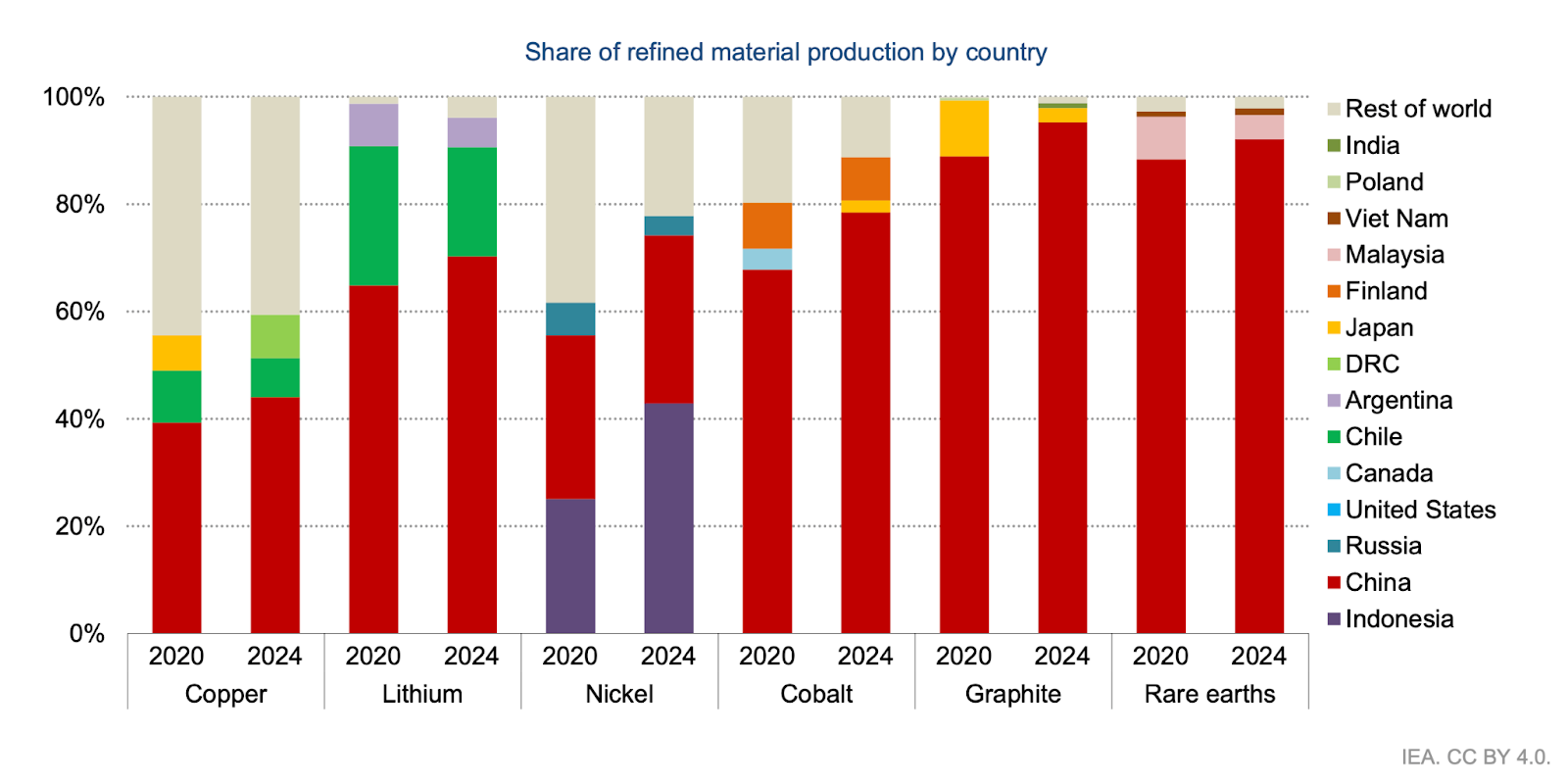

Although deep sea mining supporters still speak about how this will be a greener approach to metal sourcing, like with many other technologies, the conversation has shifted towards national security and defense. In particular, China’s domination of existing supply chains and their moves to restrict access to key metals have politicians worried about dependence on China for essential materials for both modern tech and defense.

With the increasing focus on onshoring and “friend shoring” of essential materials, critical minerals have gone from a niche field to a hot topic, with deep sea mining being put forward as a potential solution by some, including the United States government.

However, just as with the environmental impact and financial risks, the importance of processing should also not be ignored here. Even if we can efficiently harvest nodules from the deep sea, China also possesses both the vast majority of the know-how and facilities for metal processing, including ownership of Indonesian Ni refining facilities. Some countries, including the USA, actually have substantial metal reserves, but decided years ago to buy from abroad instead of processing at home, in no small part due to the dirty, environmentally harmful processes used to transform ore into metal. For deep sea mining to actually reduce reliance on China, other parts of the supply chain will also need to be addressed.

Further complicating the picture for deep sea mining companies and other new facilities, China has also shown a willingness to drop prices to undercut competitors abroad and maintain their strong position. Although governments are looking for ways to counteract such challenges, such as the newly announced Project Vault, this risk still adds geopolitical uncertainty to financial projections.

Starting in 2026?

In an ideal world, we would have enough time to carefully observe deep sea ecosystems for decades before deciding to move forward. But the real word rarely waits for complete information. Regulators are unlikely to escape making a difficult judgement call with imperfect information, particularly with the changing political landscape.

In fact, there are already signs that not all players are willing to wait for the International Seabed Authority (ISA), who are charged by the UN with regulating mining of the seabed in international waters. The ISA has been developing guidelines to ensure that marine life is protected and that royalties from mining profits are distributed equitably, but have missed several deadlines and are coming under intense pressure as the technologies needed have matured.

In April 2025, the Trump administration issued an executive order to fast-track deep sea mining at scale. Although countries have the right to mine in the exclusive economic area near their coasts, this executive order included language indicating that these processes would also apply beyond US jurisdiction, raising concerns that the US would permit companies to proceed unilaterally instead of waiting for international regulations to be ready.

Around the same time, the US subsidiary of The Metals Company officially began the process with the National Oceanic and Atmospheric Administration (NOAA) to pursue exploration licenses and commercial recovery permits in the CCZ based on the Deep Seabed Hard Mineral Resources Act of 1980. Further streamlining of the application process in January 2026 has led some to speculate that the company could begin mining in earnest as early as the end of 2026, though 2027 or 2028 is more likely.

Conclusions

It is essential that we learn to be mindful of our metal consumption and reduce our usage of these powerful, yet environmentally challenging, materials where we can. Yet without a gigantic societal shift, we will still need to source substantial quantities of new minerals for the foreseeable future.

The high concentrations of key metals such as copper, which are essential for many central technologies of the green energy transition, could make deep sea nodules a more climate-friendly source than land-based ores if choices are made carefully. But whether you are interested in the environmental impact, the financial risk, or geopolitical factors, how minerals are processed deserves far more attention than it usually receives, no matter whether the source is on land or under the sea.

With all the talk of re-shoring this essential piece of the supply chain, it is worth asking ourselves if we are truly willing to rebuild facilities that were pushed abroad years ago because of their dirty nature. If we are to build new supply chains to support polymetallic nodules or other “friendlier” sources of metals, we must seize this opportunity to build cleaner, more sustainable facilities, instead of replicating the problems of the past.

🌞 Thanks for reading!

📧 For tips, feedback, or inquiries - reach out

📣 For newsletter sponsorships - click here